Democratizing Indian Health Insurance

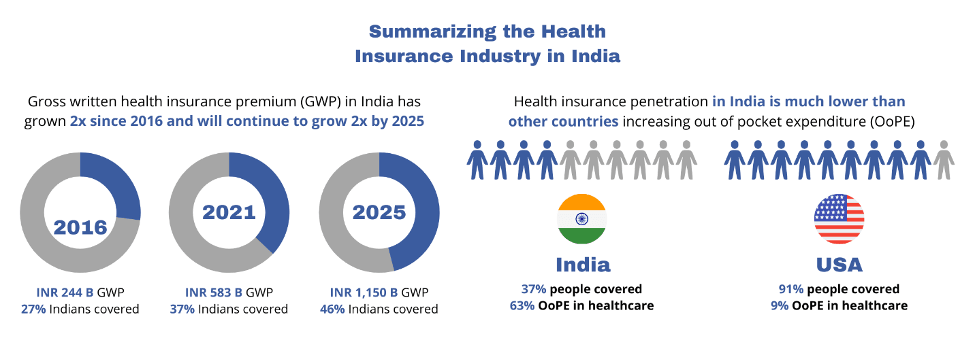

672 million Indians will be covered by health insurance by 2025, making 46% of the population insured by some form of insurance. Can technological interventions make health insurance truly accessible and facilitate 100% penetration?

Source: US Insurance penetration – US Census Bureau; US OoPE in healthcare – Centers for Medicare and Medicaid Services; Others – CRISIL Research

Why is India lagging other countries?

- Health insurance products remain complex as features like exclusions, waiting periods, deductibles, co-payments, and sub-limits are difficult to interpret

- People are behaviorally biased against spending on a future expense that might not materialize, especially at a high cost

- Policyholders have had poor claims experience leading to limited trust in insurance companies

While the pandemic has increased awareness about the need for health insurance, the billion-dollar question is how one democratizes the sector and facilitates universal penetration. For many sectors, technology has played a role in increasing access and reach. Could technology play the same role in health insurance?

Legacy players dominate the health insurance industry, with 63% of premiums channelled by five insurers.[2] However, we see start-ups beginning to disrupt the industry by optimizing costs and processes while enhancing customer experience right from purchase to claims. The Insurance Regulatory and Development Authority of India (IRDAI) has welcomed innovation by introducing friendlier guidelines like the sandbox license to pilot new products across the spectrum – distribution, underwriting, manufacturing, servicing, and claims. Novel products include ‘Friend Assurance’ that allows like-minded groups to get a policy together, ‘Reward programs’ that offer OPD services, and ‘IoT wearables-based wellness programs’ that link premium to key health indicators. These new products are finding greater acceptance than traditional ones, thus improving penetration.

We believe that three key innovation trends will shape the future of the insurance industry in India.

#1 Start-ups are manufacturing simpler and more comprehensive insurance products

While legacy carriers have lagged in product innovation, start-ups are making a space for themselves by offering coverage not only for infrequent in-patient treatments, but also for out-patient treatments, diagnostics, dental care, and mental wellness. We’re seeing the emergence of start-ups trying to build India’s version of the Health Maintenance Organization (HMO), a model widespread in the US. An HMO policyholder can only access care in a closed network of providers after a referral from their primary care physician. This results in HMO plans to have lower fees than traditional insurance products. They are shielded from high costs of claims adjudication, frauds, and overutilization of services due to the closed network. Lower fees combined with better out-patient coverage make HMO plans a compelling offering for uninsured urban middle-income households in India.

What’s next?

While insurance products have evolved, underwriting has remained static due to the lack of verified data. Today, health insurance underwriting relies on information shared by the customer.

Technology and advanced data analytics will enable better data capture and stratification of individuals basis their health-seeking behavior, medical history, and financial discipline. This vast data pool will allow insurers to underwrite policies customized to every customer providing better prices. The Government of India’s NDHM will further bolster this ecosystem. We predict that data will transform how health risks are understood, managed, and thus insured for in the coming years.

#2 Technology is making insurance distribution faster and easier

Policy Bazaar, with its INR 562 billion IPO, has become synonymous with new-age insurance distribution. In its shadows, are other impressive start-ups making insurance distribution efficient for both individuals and corporates.

Individual health insurance distribution has been an agent-driven model for years. 75% of the retail health insurance premium was channeled through agents in 2020 and only 2% was via digital sale.[3] Due to this unfettered dominance, many start-ups have adopted an agent-led model to reach consumers. Start-ups are attracting agents by providing them access to a variety of insurance products offered by several underwriters, real-time issuance, upskilling courses, and policy and claims management support.

On the other hand, the group insurance distribution market also remains competitive with every broker vying for a share of the 11 million+ MSMEs. The competition and the bargaining power with corporates have made commissions average around 7.5% of the premium channeled. Some start-ups are differentiating themselves by providing HR managers with dashboards with insights on claims and usage analytics, and employees with engagement platforms, out-patient clinical services (such as a tele-visit with your doctor), concierge services, and claims assistance. Others are making health insurance more comprehensible for customers on digital platforms.

What’s next?

There is still a huge opportunity for digital platforms to educate the customer through a content-led approach and enable a digital purchase.

What is also exciting is the inception of IaaS (Insurance as a Service) players enabling anyone to distribute insurance. Today, several cooperative banks, and HealthTech and WealthTech players are vying to increase their monetization avenues by selling health insurance. This has shot up the demand for IaaS players. IaaS providers can allow even non-insurance players to sell insurance without burdening their resources in procuring a license or making partnerships with insurers.

#3 Recognizing that claims management is the biggest pain point for policyholders, start-ups are leveraging tech integrations to address it.

Traditionally, claims adjudication is a fairly man-power intensive service. Delays in getting claims, receiving only partial payments, and lengthy procedures create a trust deficit between customers and insurance providers. Start-ups are aiding policyholders by educating them on inclusions and exclusions, decoding bills, filing claims, and helping finance any upfront cost. This is often done through a patient mobile app that allows them to seek information on procedures, upload their medical and policy documents and file a claim with the insurer.

What’s next?

A disruptive change that will truly transform the industry is the emergence of models connecting hospital EMRs with insurers for real-time automated claims management. Despite the multiple legacy systems hospitals operate on, the burgeoning innovation landscape offers hope for such a disruption providing policyholders with a faster claims experience

All in all, the insurance industry, believed to be archaic, laggard, and resistant to change, has captured the fascination of both innovators and entrepreneurs. The last few years have seen some game-changing start-ups beginning to disrupt the status quo. Companies like Acko, PolicyBazaar, and Digit are already well-established unicorns, while many other start-ups are progressing towards an inflection point.

Better insurance products, universal distribution, and improved technology infrastructure are changing the health insurance landscape in India. These new-age ideas could make consumers emerge as the true winners from the insurtech disruption.

Authors: Dr Pankaj Jethwani, Namit Chugh and Vedika Tibrewala

Link to the Article:

https://health.economictimes.indiatimes.com/news/insurance/democratizing-indian-health-insurance/90142396